Ценовая статистика

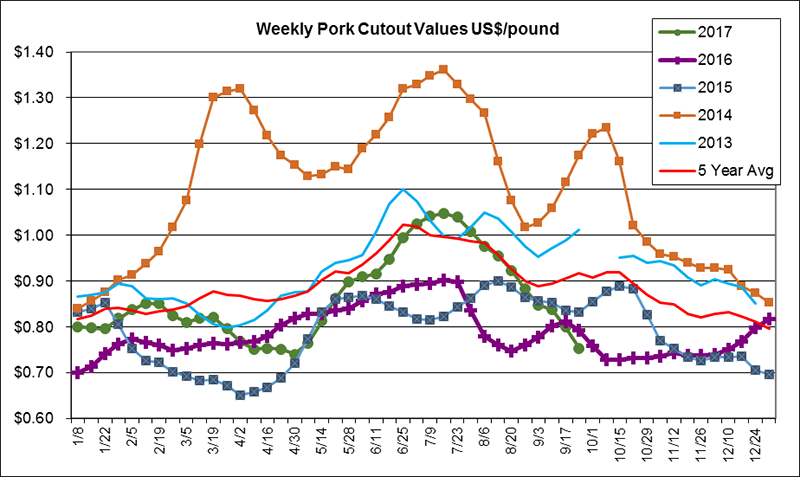

The pork cutout trended higher from May thru mid-July as U.S. demand for bacon, sausages & cuts for grilling along with strong exports drove prices up but has since been trending lower, and for wk ending Sept 22, it was down 5% yr-over-yr to $0.75/lb. Bellies were a main contributor to summer’s higher pork prices, reaching record levels in mid-July, but have since been dropping, and are now 3% below last yr. For Sept 22 wk, picnics were $0.58/lb., + 13% yr-o-yr, and values were higher for ribs ($1.20, +5%), but lower for hams ($0.63, -1%), belly ($0.97, -3%), loins ($0.79, -10%), and butts ($0.87, -17%); the wholesale prices for derind bellies ($1.81, +9%) and tenderloins ($2.30, +6%) were higher yr-o-yr, & bnls sirloins were even ($1.15). Heavy bone-in hams ($0.61, -1%), cushions($1.07, -5%), St. Louis spareribs ($1.86, -11%), bnls butts ($1.20, -13%), & loins ($0.93, -20%) were down.

Cash hog carcasses were $0.56/lb on Sept 25, down 1% as hog prices dipped below yr-ago levels for the 1st time since May. Oct. lean hog futures contract has been trending lower since mid-Aug, with Dec & Feb contracts trading sideways in Sept, while the April contract trends higher (Sept 28 CME Lean Hog Futures closing contract prices with change from July 24): Oct: $55.55 (-$10.90), Dec: $58.28 (-$2.90), Feb: $63.35 & Apr: $68.45.

USDA’s quarterly Hogs & Pigs report, Sept 28, shows continued expansion in the U.S. pork industry. Like the last report, both the total hog inventory and the market hog inventory were record large for the quarter, with total hogs up 2%, market hogs up 3%, & breeding hogs up 1% from 2016. Productivity cont. to gain with June – Aug pig crop at records (33 mill hd), up 2%, & pigs saved per litter was record high at 10.65. Like 2015/2016, USDA expects production to set new records in 2017 and 2018. 2017 production should be 11.72 mill metric tons (MT), up 3.6% and 2018 is expected to be 12.12 mill MT, up 3.4%.