Price trends of the pork market in early 2018 published

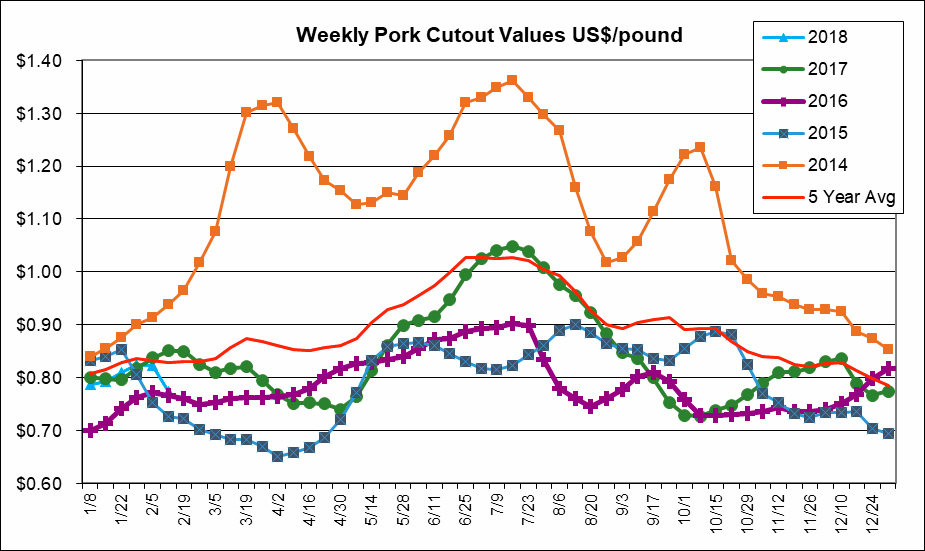

In Jan, the cutout trended higher and was similar to 2017 levels before it dropped in Feb. For the wk ending Feb 9, the cutout was $0.77/lb., down 9% from 2017, but higher for picnic ($0.52/lb., +12%), butt ($0.89, +11%), and rib ($1.32, +9%), while lower for loin ($0.72, -4%), ham ($0.58, -7%), and belly ($1.28, -29%).

Picnic & butts should be moving seasonally lower into Feb. Loins and tenderloins trended higher the last two wks. Heavy B-I hams were strong in Jan, then dropped 18% from the wks Jan 26 to Feb 9. For wk ending Feb 9, wholesale values were higher yr-over-yr for St. Louis spareribs ($2.10, +12%), med. trimmed spareribs ($1.37, +8%), bnls butts ($1.18, +6%), and picnic cushion ($1.04, +4%), while lower for loins ($0.87, -1%), tenderloins ($2.12, -3%), bnls sirloins ($1.02, -4%), bnls rollout hams ($1.16, -4%), heavy B-I hams ($0.57, -6%), & derind bellies ($2.43, -9%).

Cash hog carcass prices have been above yr-ago levels since last Oct, as additional plant capacity supported prices; they were $0.73/lb for wk ending Feb 10, up 2% from 2017. Lean hog futures contracts trended lower through Jan (Feb 15 CME Lean Hog Futures closing contract prices with changes from Jan 8): Apr: $69.73 (-$7.07), May: $75.90 (-$5.05), June: $80.20 (-$5.30), & July: $81.32.

Pork production was up 2.6% in 2017 to a record 11.60 mill Metric Tons, and should set a record in 2018, with USDA’s Feb forecast at 12.19 mill MT (up 5.1%) (and thru 1st wk of Feb, up 2.2% from last yr).

SOURCE: USMEF